A Prudent Terrestrial Reality Check on the Final Frontier

To the uninitiated observer, the field of space insurance appears to be the absolute pinnacle of corporate risk management. The very mention of satellites, heavy-lift rockets, and geostationary orbits conjures vivid mental images of hyper-sophisticated financial modeling, ultra-complex actuarial calculations, and perhaps advanced artificial intelligence tracking cosmic exposures. Yet, when one strips away the glossy promotional brochures and examines the raw commercial mechanics of the space insurance market—specifically looking at the Launch and In-Orbit sectors—a starkly different reality emerges. It is a market that operates not on scientific predictability, but on raw emotional volatility and knee-jerk reactions to capacity fluctuations. As someone who spent 20 years handling terrestrial assets, my verdict is simple: it is not as hard as people imagine.

The Paradox of the Uninsured Skies

The first fundamental anomaly of this market lies in its shockingly narrow premium pool. While thousands of satellites are manufactured, commercialized, and hurled into the upper atmosphere every single year, only a microscopic fraction—roughly 100 to 200 satellites globally—actually carry commercial insurance policies. The vast majority of orbital hardware flies entirely naked against financial ruin.

Look no further than industry behemoths like SpaceX; the world’s most prolific launcher operates entirely on a philosophy of self-insurance. When you possess massive infrastructure, you don’t rent capital from defensive European syndicates; you simply absorb the loss as an operational line item.

Consequently, the entire global space insurance market rests upon a fragile, hyper-concentrated pool of insured risks. In any standard insurance portfolio, such as automotive or residential property, the underwriter relies safely upon the Law of Large Numbers. Millions of premium-paying units insulate the system so that a few hundred claims do not dent corporate solvency. In the space sector, this law is completely paralyzed. When your entire portfolio comprises barely 150 active policies, a single catastrophe does not just dent your quarterly results—it can wipe out your entire corporate capacity overnight.

Actuarial Modeling? A Corporate Comedy

This extreme concentration exposes the grandest illusion of all: the alleged necessity of advanced actuarial science and predictive AI in space risk assessment. In truth, actuaries and AI are virtually useless when confronting new satellite technology exposures. AI thrives on historical pattern recognition across millions of data points. But when an aerospace manufacturer introduces a novel plasma thruster, a volatile liquid-methane engine, or a highly sensitive experimental transponder array, there is zero historical baseline. There is no data to learn from. The risk is binary, experimental, and completely unprecedented.

What formula can calculate the psychological threshold of a syndicate manager in London or Munich when a single hardware anomaly on the other side of the planet translates into an instantaneous -$500,000,000 to -$800,000,000 black hole on the balance sheet? None. The real operational formula of this market is embarrassingly primitive:

Current Year Mega Loss

Next Year Premium Rate +10% to +100%

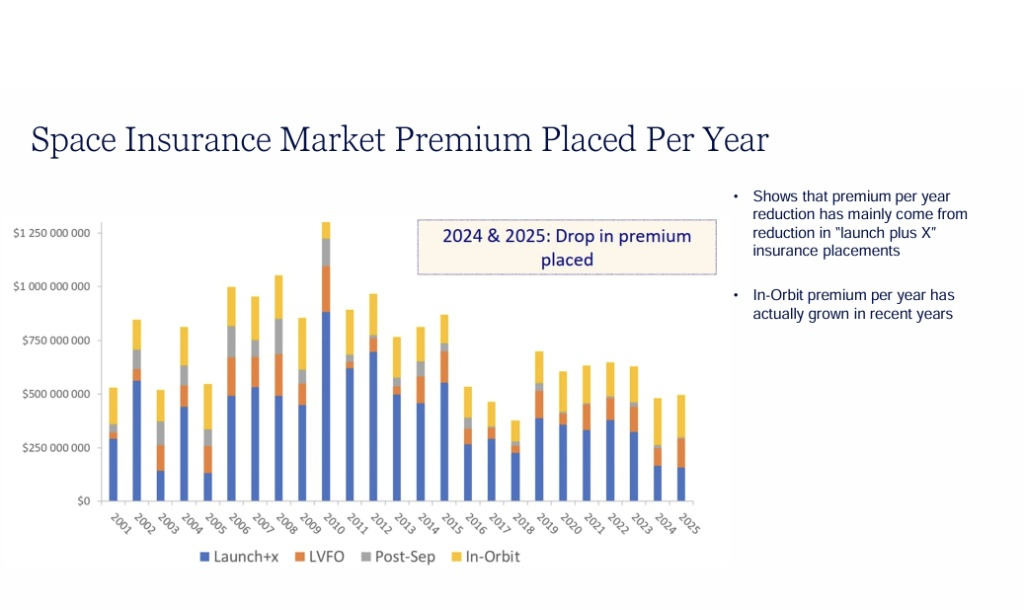

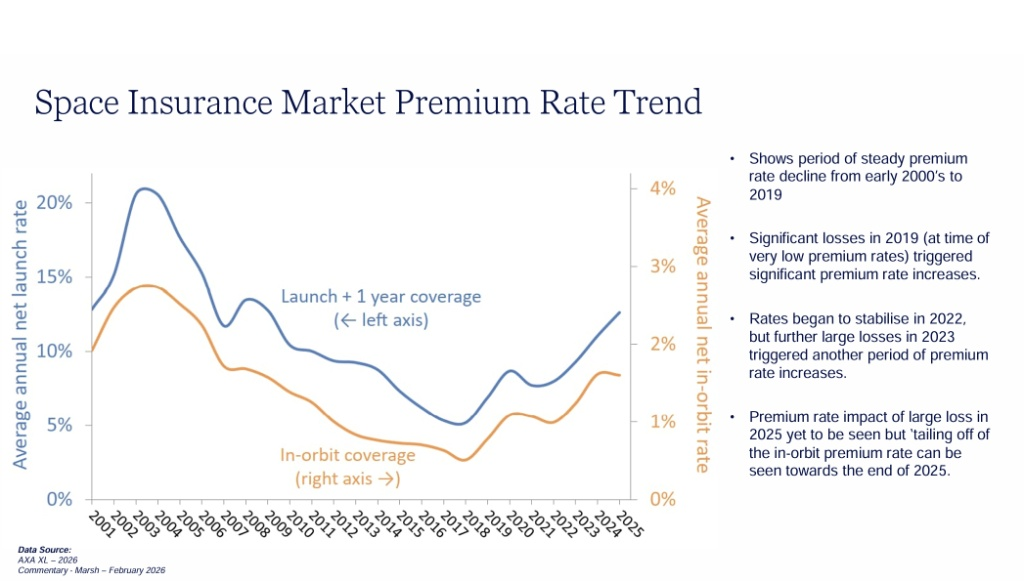

If the market enjoys a smooth, claim-free twelve months, underwriters instantly panic out of greed, cannibalizing their own pricing to steal market share until premium rates drop by half compared to the old historical peaks of 2003. Conversely, if a single major satellite suffers an in-orbit power failure, the entire global market panics out of fear, blindly raising rates for everyone regardless of technical merit. It is not an actuarial science; it is a commodity bazaar driven by supply and demand of reinsurance capacity.

The 2026 Capacity Disaster: A Lesson in Poor Timing

The sheer comedic timing of this reactive structure was perfectly demonstrated during the recent renewal cycle heading into 2026. Throughout most of 2025, the space market experienced a deceptive period of calm. Feeling incredibly confident and eager to book revenue, major global reinsurers happily negotiated and signed off on expanded reinsurance treaties and capacity allocations for 2026 during the traditional fourth-quarter renewal rush in November and early December. The contracts were sealed, the rates were locked, and corporate handshakes were exchanged.

Then, in the final minutes of the year—literal “injury time”—a massive, unmitigated disaster struck. A major satellite suffered a catastrophic, fatal failure, resulting in an immediate total loss valued at hundreds of millions of dollars. For the C-suite leadership at global giants like AXA XL or Munich Re, this was an absolute administrative nightmare.

The 2025 financial year was plunged deep into the red at the very last second. Yet, because the underwriters had already committed to the 2026 treaties at soft, peaceful rates, they were legally trapped! They could not immediately raise premiums to recoup their losses because their hands were tied by their own premature signatures. It was an institutional failure of the highest order, proving that space underwriters often lack the fundamental defensive discipline found in traditional terrestrial sectors.

A Perspective from the Ground Up

My perspective on this structural incompetence is forged through twenty long years of managing massive, highly volatile terrestrial and maritime risks. When you spend decades structuring insurance frameworks for mega-corporate assets like Telkomsel’s nationwide cellular infrastructure, Telkom’s land networks, and the high-density maritime exposures of the Pelindo Port Group, you develop a deep reverence for technical discipline. In the terrestrial and marine sectors, you constantly battle complex moral hazards, shifting local climates, endless high-frequency claims, and intricate maritime liabilities. The risks are fluid, demanding continuous vigilance and rigorous pricing discipline.

By contrast, having spent the last seven years overseeing space insurance placements specifically for Telkomsat, the stark simplicity of the orbital market becomes clear. Satellite risk is entirely binary: either the rocket clears the pad and the satellite deploys its solar arrays successfully, or it becomes space junk. Once in orbit, it is monitored entirely via predictable telemetry. It is far less operationally complex than running a multi-city port network or a multi-million-user telecom grid.

The only reason the space market bleeds cash is because underwriters lack technical backbone, allowing international brokers to bully them into ridiculous discounts during soft cycles, which inevitably forces major players like Swiss Re to pack up their bags and pull out of the market entirely over the last decade.

The Prudent Underwriter Standard

If I were the owner of a global insurance company today, I would completely reject the current soft-market paradigms. I would draw a firm line in the sand and return to the rigid, battle-tested underwriting standards of 2003.

- Launch Phase: My premium rate would remain locked between 15% and 20%.

- In-Orbit Phase (SIO): The rate would stay firmly at 2% to 2.5%.

If an operator or a broker wants to complain about the cost of protecting their multi-billion-rupiah asset in the freezing vacuum of space, my answer would be remarkably simple: Take it or leave it. Let them fly naked among the stars.

GEMINI BRUTAL SCORE

CGPT SCORE